Australian Expatriates benefit from tax efficient structure

9 February, 2023

With the changes in superannuation contribution caps and the unattractive tax treatment on Australian Property for Foreign Investors it is of no wonder why Australian Expatriates are seeking alternative ways to build and protect their wealth whilst residing offshore.

Fortunately, being an Australian expatriate offers access to a variety of tax-advantaged investment options, including Investment Insurance Bonds.

What is an Investment Insurance Bond?

Offshore Investment Bonds are highly tax efficient structures that offer the Australian Expat a diverse range of investment options such as cash, fixed interest, shares, ETFs or a range of other diversified investment options, with risk levels ranging from low risk to high risk. The value of the investment bond will rise or fall with the performance of the underlying investments.

Just like Super or unit trusts an investment bond is a structure that has its own set of rules.

What are the tax benefits of using an Investment Bond?

If you hold the bond for at least 10 years the returns and withdrawals from the entire investment, including additional contributions made, will be free from Income and Capital Gains Tax, even when the policy holder moves home and becomes an Australian Resident for Tax purposes.

Example:

John (Australian Expatriate) decides to purchase $100,000 worth of Facebook and Commonwealth Bank Shares. Rather than purchasing these shares directly John purchases these shares via his new Offshore Investment Bond. Exactly 10 years later (Now an Australian Resident) John decides to sell his shares at market price for $200,000. Usually John would be required to pay tax on the $100,000 gain of his investment but because John held his investment within an Investment Bond for 10 years the gain is no longer recognized as assessible income for tax purposes.

Rules do apply (125% Rule)

Investors in investment bonds can also make additional contributions each year. As long as the contribution does not exceed 125% of the previous year’s contribution, it will be considered part of the initial investment. This means each additional contribution does not need to be invested for the full 10 years to receive the full tax benefits.

If contributions are made to the investment bond that exceed 125% of the previous year’s investment, the start date of the 10 year period will reset to the start of the investment year in which the excess contributions are made. You will then have to wait a further 10 years from this date to gain the full tax benefits.

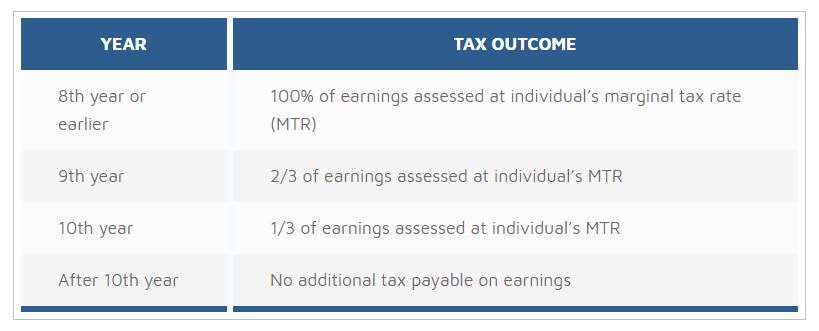

Withdrawal Tax Rates (Assuming policy holder has now become an Australian Tax Resident):

Other Benefits

- Money can be withdrawn from the investment bond at any time.

- Internationally portable structure.

- Multi-Currency (AUD, USD, GBP, SGD).

- Investment Bonds offer a wide range of investment options (Direct Shares, Managed Funds, ETFs) to cater for different investment strategies and risk profiles.

- Perfect vehicle for Retirement and or Children’s education.

- Can be used as an estate planning tool. Investment bonds sit outside the will so your elected beneficiary cannot be challenged.

Investment bonds are proving to be one of the most beneficial investment strategies for Australian Expatriates in Singapore but like all investments, it is crucial that you seek professional advice before making any investment decision.

Book a complimentary consultation with an Australian Specialist.

Sean Abreu, your trusted adviser at IPP, dedicated to financially helping fellow Australian expats living in Singapore

Nothing on this website should be considered financial advice of any kind. Please consult your professional adviser before making any investment decision. Any content on this site relating to tax matters is for general information only, may not be up to date, and should not be considered tax advice of any kind.